Publisher:

Bonnie King

CONTACT:

Newsroom@Salem-news.com

Advertising:

Adsales@Salem-news.com

~Truth~

~Justice~

~Peace~

TJP

Jan-29-2013 10:55

TweetFollow @OregonNews

TweetFollow @OregonNews

An Apology for JP Morgan Chase or

Dimon Is The Street's Best Friend

Salem-News.com

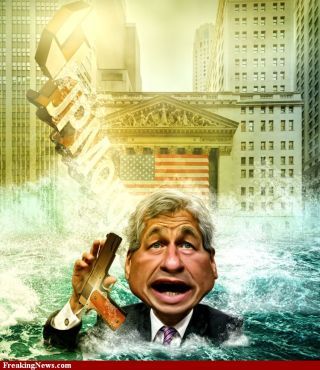

What, even in Wall Street circles, could be more transparent?

Courtesy: www.freakingnews.com |

(DAYTONA BEACH, FL) - In the merry month of May, a brace of headlines twitterpated the financial world, one out of romantic Italy, the other on the Street of Dreams, both dealing with the venerable bank/dealer/trader/broker with the curious amalgam of the oldest family escutcheon on Wall Street and the sainted institutional name that chases as well as being chased, and is currently, as always, anything but chaste.

Also figuring in this lumbering pas de deux was another financial titan known as the Institute For Religious Works, which may sound like an international ladies' aid society but is in fact that giant, mysterious and unknowable institution, even shadier than its Wall Street counterparts – The Vatican Bank.

The first – and funniest – story is that in its Milan office in Italy, JPMC (I'm getting tired of spelling it out) had fired, expelled and cast out from its financial temple the ultimate money-changer (or at least the account of) the above-mentioned Vatican Bank. The reason, the Chase guys suggested? Lack of transparency, which is to say a lack of information about the holy banco's transactions. There is apparently nothing quite as morally upright as an earnest pot in the process of calling a kettle – even an ecclesiastical one - black.

That was startling enough. But a day or so later, a chastened (pun intended) Chase Chairman, Jamie Dimon (French pronunciation like “demon,” unlike a girl's best friend) announced in New York that his venerable institution had just taken a bath to the tune of $2 billion in its trading operations. (No connection with its Italian proclivities.) He offered this news in a contrite fashion, pleading transparency, and sounding like an apology, which well it might have, given that JPMC, in addition to its other financial activities is a deposit -taking institution and therefore the two bills that evaporated could be construed to be somebody else's (i.e. depositors') money.

Moreover, and perhaps even moreunder, the $2 billion glitch has since mushroomed to six or seven, with the further information that the deal hasn't yet been unwound. Definitely, as the chaps in the Holy See describe it, not transparent. (Holy See, holy do.) Briefly, the trading operation in question occurred as a result of a hedge operation involving derivatives and a bond index, but I suggest you don't try to understand the details. I landed on Wall Street 62 years ago, and I've been pretty well knocking around its periphery ever since, and I still can't fathom this stuff.

But in broad strokes, it appears that two separate entities in the bank's trading operation, one in London, were on opposite sides of a mammoth trading operation in C19's, an esoteric financial cocktail involving bets against an investment-grade bond index. Which sounds roughly like a Dickensian pickpocket in the employ of Bill Sykes dipping into the boss's wallet.

In order to render transparent this murky story, it appears that all the hedge funds from New York to London's fair City ever since have been circling the hapless megabank, taking positions and snapping at the edges of JPMC's still unwound inventory like a school of nurse sharks surrounding a bleeding great white.

- JPMorgan Chase's trades were built around contracts tied to corporate bonds. Specifically, their traders sold huge amounts of protection on an index of 125 highly rated corporate bonds. Simply put, if you're simpleton enough to believe in this stuff, JPMorgan Chase's massive trade stood a better chance to pay off if the markets had continued to rally. They didn't. The principal bet was on an index, known as IG9, of 125 American investment-grade companies, such as J.C. Penney, insurer MBIA and its counterpart Radian. And that play had recently absorbed king-size hits last week, driving up the cost of offering protection against a default.

- In addition, since Dimon's mea culpa, more hedge funds have piled into the index, further driving up the cost of selling protection, a process that is likely to continue, further expanding the bank's losses.

- "Part of the problem of what they were doing,” said one Street observer, (from a safe distance) “is that they were too big in the trade to be able to trade out of it." Penny stock dynamiters learned this simple principle years ago – once you own a majority, who is there left to hustle?

Such is the Wall Street we have come to know and love. But Jamie Dimon, who has the reputation as one of the straightest shooters on the Street (as in Wyatt Earp and Billy the Kid) is scheduled to clarify everything shortly when he will testify before the Senate Banking Committee.

Commented Alan Abelson, Barron's acerbic columnist: “Our advice to Jamie Dimon when he testifies: don't use words of more than one syllable, speak fast, and go heavy on the sincerity schtick.”

Meanwhile, back in Rome, where all roads used to lead, the Vatican has been threatening to take legal action against those publishing a new book of leaked internal documents which definitely render more transparent the power struggle and corruption inside the Holy See and the tribulations of the besieged top banker, Ettore Gotti Tedeschi (presumably no relation to Jake Gotti of the New York family), who reports regularly to the Chairman in the gold dress.

- Il Papa has already appointed a commission of cardinals (CoC) to investigate these “Vatileaks.” The Holy See has seen fit to take such measures to counteract rumors concerning its shortfall in complying with international anti-money-laundering norms, which are suspect at the best of times, not to mention the worst of times. According to Vatican sources, possibly a disgruntled Swiss Guard, a recent transparent Italian newspaper article violated the Pope's right to privacy. I mean, you can't have transparency and papal privacy at the same time, can you?

- A Holy See spokesprelate, Reverend Federico Lombardi vowed to get to the bottom of the stolen documents, averring that the Holy See will see to it that justice will be done, appealing to international cooperation if necessary. Their international reputation has been that solid recently.

An intriguing sidebar, in those letters, the administrator begged not to be transferred for having exposed corruption that cost the Holy See (which had seen enough by this time) millions of Euros in higher contact prices. No dice. The admin, Monsignor Carlo Maria Vigano received the ultimate demotion from a sinecure in the Instituto. He was banished to darkest Washington as U.S. Ambassador.

The banco vaticano has been trying for years to burnish its image as a shady tax haven beset by scandals. One of them is the collapse of Italy's Banco Ambrosiano and the death of its head, Roberto Calvi, asset manager for Vatican investments, found hanging from London's Blackfriars Bridge several years ago, possibly supplying the screen play idea for Godfather III. And of course since then, we've all witnessed Al Pacino, in the latter's title role, switching his main house account to the Instituto we have come to recognize as next to Godliness.

What, even in Wall Street circles, could be more transparent? These heavy corporate banking concerns have weighed heavily on the Pontiff, scarcely allowing him any time for penance and prayer, let alone ministering to his 800 million-strong flock.

Joe the Rat, as you are known in the Sicilian hierarchy, are chief stockholder and chairpope of the board, of course. We who are about to be overdrawn salute you in true Caesarian fashion for being so transparent – we've been seeing through you for a long time now.

By comparison, Jamie Dimon has it easy. I doubt if he even goes to Mass. But he'll have his day with a Senate Committee sooner or later. And it'll all be as transparent as Fox News can make it.

Bill Annett grew up a writing brat; his father, Ross Annett, at a time when Scott Fitzgerald and P.G. Wodehouse were regular contributors, wrote the longest series of short stories in the Saturday Evening Post's history, with the sole exception of the unsinkable Tugboat Annie.

At 18, Bill's first short story was included in the anthology “Canadian Short Stories.” Alarmed, his father enrolled Bill in law school in Manitoba to ensure his going straight. For a time, it worked, although Bill did an arabesque into an English major, followed, logically, by corporation finance, investment banking and business administration at NYU and the Wharton School. He added G.I. education in the Army's CID at Fort Dix, New Jersey during the Korean altercation.

He also contributed to The American Banker and Venture in New York, INC. in Boston, the International Mining Journal in London, Hong Kong Business, Financial Times and Financial Post in Toronto.

Bill has written six books, including a page-turner on mutual funds, a send-up on the securities industry, three corporate histories and a novel, the latter no doubt inspired by his current occupation in Daytona Beach as a law-abiding beach comber.

You can write to Bill Annett at this address: bilko23@gmail.com

|

|

|

Articles for January 28, 2013 | Articles for January 29, 2013 | Articles for January 30, 2013

Salem-News.com:

Terms of Service | Privacy Policy

All comments and messages are approved by people and self promotional links or unacceptable comments are denied.

[Return to Top]

©2026 Salem-News.com. All opinions expressed in this article are those of the author and do not necessarily reflect those of Salem-News.com.